CHEERS TO

Planning and prioritizing for a better future

Day-planners. Calendars. Sticky notes. You likely make some sort of plan to help you make tradeoffs and balance your life today. But what about your life tomorrow? Building a financial plan is even more important because it helps you make informed choices between your obligations and goals, and gives you the flexibility to adjust course as new situations arise. Some important steps for building a plan include:

- Understand where you are today and tomorrow

- Explore your goals (and what they may cost)

- Make informed tradeoffs

Understand where you are today and tomorrow

You need to know your current financial picture in order to explore what's possible in the future. A first step is figuring out your net worth, which is the result of subtracting your liabilities from your assets. To calculate your net worth, you'll need to consider all of your accounts, including:

- Checking and savings

- Investment and brokerage accounts

- Retirement accounts

- 529 college savings accounts

- Real estate

- Cryptocurrency holdings

- Student loans

- Mortgages

- Credit cards

Then you need a solid understanding of your cash flow, including your income, spending and savings. This information can help you plan your monthly and annual savings.

To project your future finances, consider any upcoming big expenses or windfalls that could shift your overall outlook and expected savings. Accurate projections also require incorporating factors like investment returns, inflation, income growth and taxes, among others.

This probably sounds like a lot to do, but all of this information is necessary to determine how close you are to achieving your goals.

Let technology do the heavy lifting.

Our free planning app calculates your net worth, projects its future value, and automatically updates as things change.

Explore your goals (and

what they may cost)

You know best which goals are most important to you. These can be life milestones, like buying a home or covering a child's college costs, or other pursuits such as taking a sabbatical from work to travel.

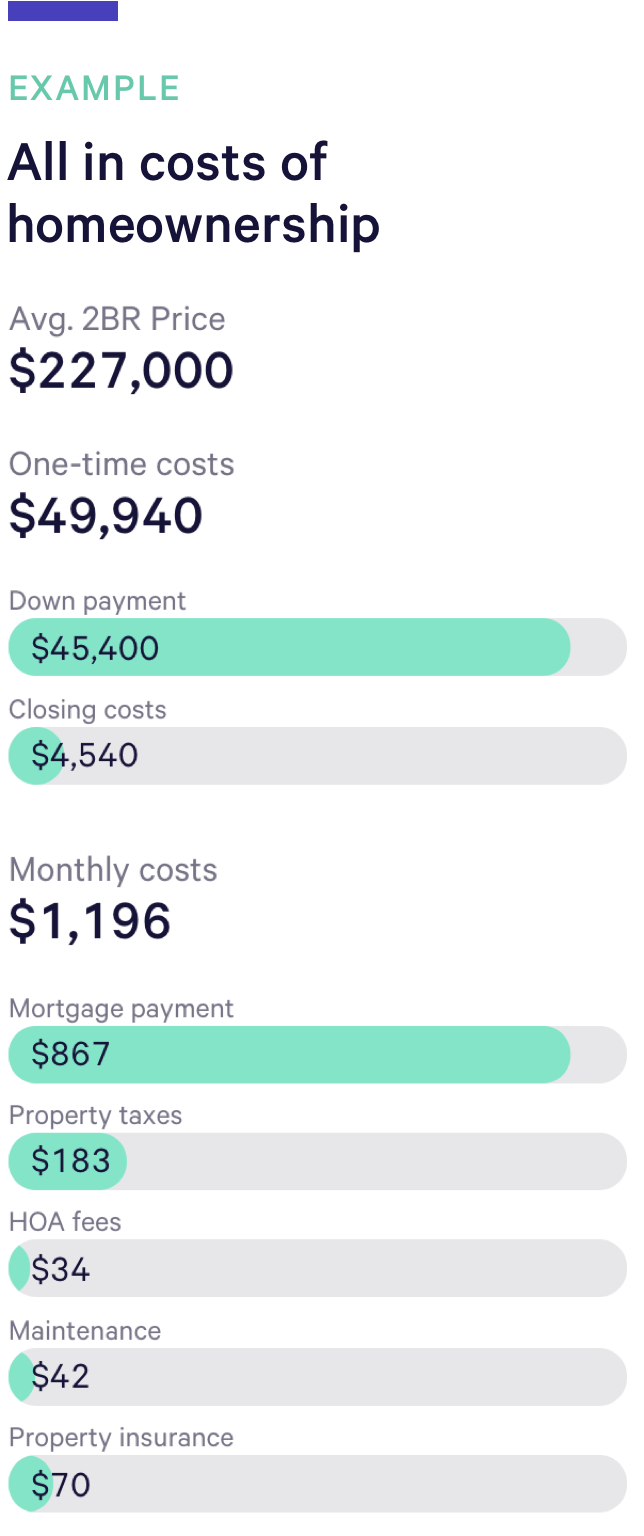

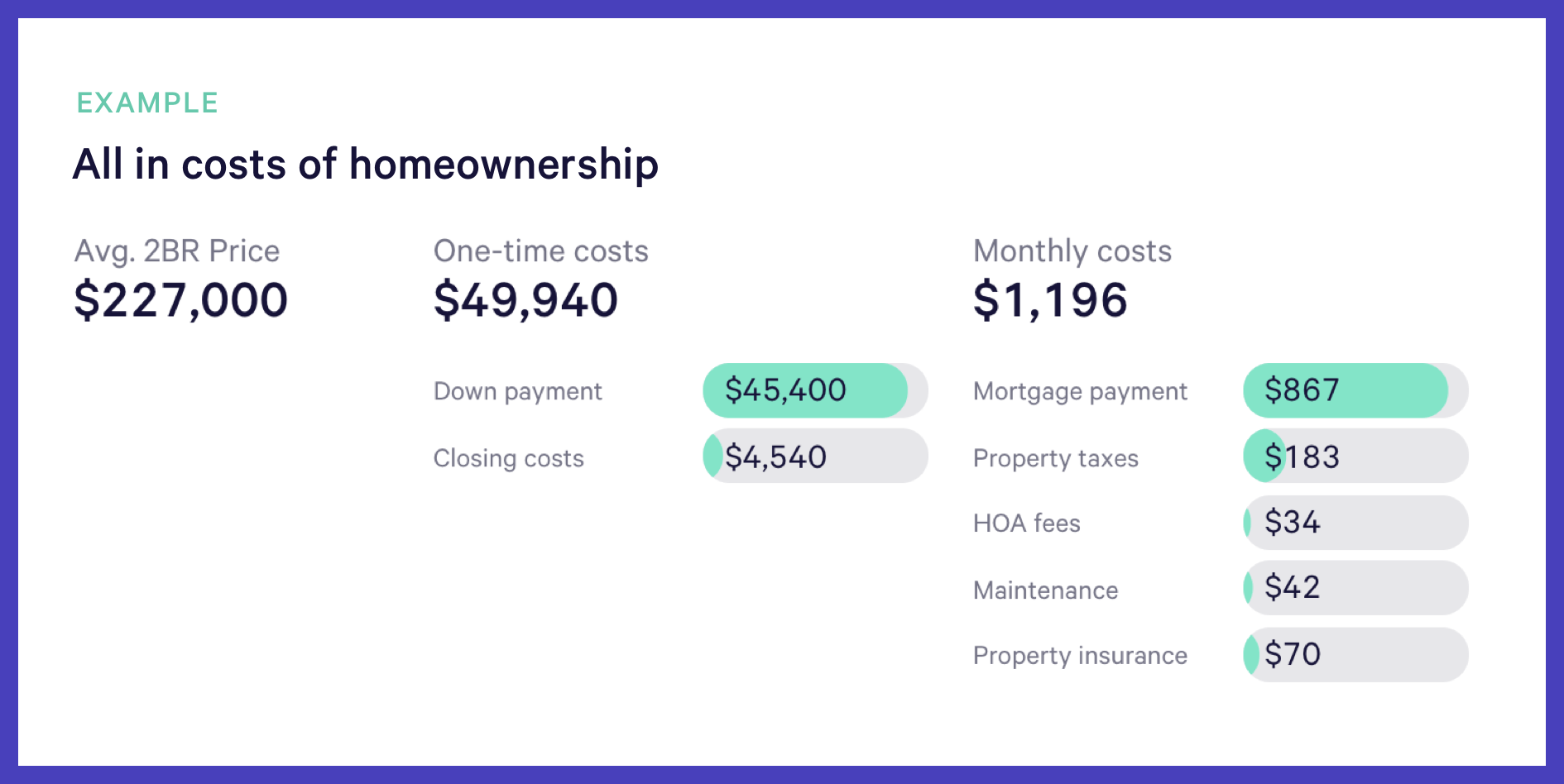

Each goal will have its own set of costs, and that may be more than just the sticker price. For example: when buying a house, not only should this calculation include the downpayment and monthly mortgage costs, but it should also include expenses such as property taxes, insurance and closing costs.

Source: Wealthfront Research based on data from Redfin, the American Housing Survey, and the American Community Survey. Planning for a home? We cover the essentials in our Home Guide.

In some situations cost might be more than just dollars and cents — you may need to assess the relative risk and reward of each scenario. For example, if you plan to take time off work to earn a graduate degree, the increased salary you'll earn with that degree might outweigh the hefty tuition and loss of income while you're in school.

After understanding the costs and risks, calculate whether you can afford your goals on a given timeline by comparing how much you can realistically save (and how much those savings will grow to) with the future all-in expected costs. Some factors to consider are whether your goal is a one-time or ongoing expense and how far into the future you expect to achieve these goals.

Mapping out this affordability gives you the information to decide if you need to make adjustments in order to reach your goals. Curious to see how we approach doing this exercise for retirement? Read more →

More resources

Make informed tradeoffs

You may have competing financial priorities, from near-term purchases to planning for retirement. Guess what — you're not alone! Turns out many people try to reconcile buying a home now and having enough to retire in the future.

Depending on your situation, there are a number of levers you can adjust to try and achieve a particular goal. For a home purchase it might be:

- Cut back on how much you are spending today (save more)

- Plan to buy a home a year later (change goal timeline)

- Aim for a smaller home or cheaper location (change goal cost)

- Or perhaps you adjust one of your other goals, like not taking the 6-month world trip you had in mind.

Exploring these different scenarios will help you land on the tradeoffs that you should make. It's important to be realistic about what's possible. One of the benefits of identifying goals and proactively building a plan is you'll understand what you actually can do, which hopefully makes you feel more confident and in control of your future. And as new circumstances change or new goals pop up — as they inevitably do — you can revisit your plan and make adjustments.

More resources

TO SUM IT UP

We believe the best way to know if you can afford something is to have a comprehensive plan. Review your overall financial picture, chart your goals, and prioritize what's important. Knowing the true affordability of a goal will empower you to achieve it!

Dive into another question →